Economy

The construction industry regularly goes through cycles of ups and downs, influenced by various economic, political and social factors.

Construction companies today find themselves in an enormous field of tension. Overregulation and the high building standards, for example in the area of energy efficiency, are a heavy burden. In addition, there is a shortage of skilled workers and a scarcity of materials and raw materials, which leads to supply bottlenecks and consequently to construction delays. All this makes building expensive. At the same time, affordable housing and green cities are to be realised.

Global Risks Report 2025 - The younger people are, the greater their fear of economic downturn

Published

10/2025 by Team buildData

This year (2025), we are a little late with our brief analysis of the World Economic Forum’s Global Risks Report 2025. It contains some interesting detailed changes to the global community’s assessments compared to previous editions, although in the 10-year outlook, the top rankings remain more or less unchanged in terms of topics.

In its current outlook for the next 10 years, the global community assesses the risks associated with climate change as high. This assessment has been a continuous trend for more than 10 years. The risk of failing to meet climate targets is consistently ranked among the top 5 global risks.

In the current and forward-looking rankings for 2 to 10 years, this is reflected in the increasing fear of extreme weather disasters and the resulting environmental and economic consequences. In the outlook for 2025 +10 years, the top four positions are consistently occupied by environmentally relevant topics. As mentioned, the topic ‘Extreme weather events’ ranks first, followed by ‘Biodiversity loss and ecosystem collapse’, ‘Critical change to Earth systems’ and ‘Natural resource shortage’.

As the future draws nearer, however, the rankings show that the global community is being overtaken by current issues and environmental issues are temporarily losing focus. Examples include the global pandemic in 2021 and the current wars in Ukraine and Palestine and their consequences (inflation, energy supply, food).

While the fear of ‘extreme weather events’ is already ranked as the second-biggest risk by the global community, people are currently more focused on issues such as armed conflicts between states, global economic conflict, cyber espionage and cyber warfare, misinformation and disinformation, and increasing social polarisation. This is clearly a reflection of the current geopolitical tensions and the mutual hybrid military and non-military attacks.

The current Global Risks Report 2025 provides an interesting breakdown by age group. It highlights in particular that the younger generation ranks the risk of economic downturn and the associated risk of personal economic decline among the top three risks. In summary, it can be concluded that the younger people are, the greater their fear of economic downturn.

For people under the age of 50, this also applies to the topic of ‘lack of economic opportunities’. The under-30s are the only group to vote for the risk of decline in health and well-being.

Globally, the risk of economic downturn ranks among the top risks in the following regions: Latin America, North America, Oceania, South-Eastern Asia and Southern Asia. But even in the USA, the UK and emerging economies such as Brazil, respondents consider economic downturn to be one of the greatest risks.

The World Economic Forum's Global Risks Report is based on the Global Risks Perception Survey (GRPS), which was conducted in autumn 2024. The global risk landscape is compiled by over 900 experts from academia, business, government, international organisations and civil society. A global risk is defined as the possibility of an event or situation occurring that, if it did occur, would have a significant negative impact on a substantial portion of global gross domestic product, population or natural resources. The Global Risks Report 2025 is now in its 20th edition.

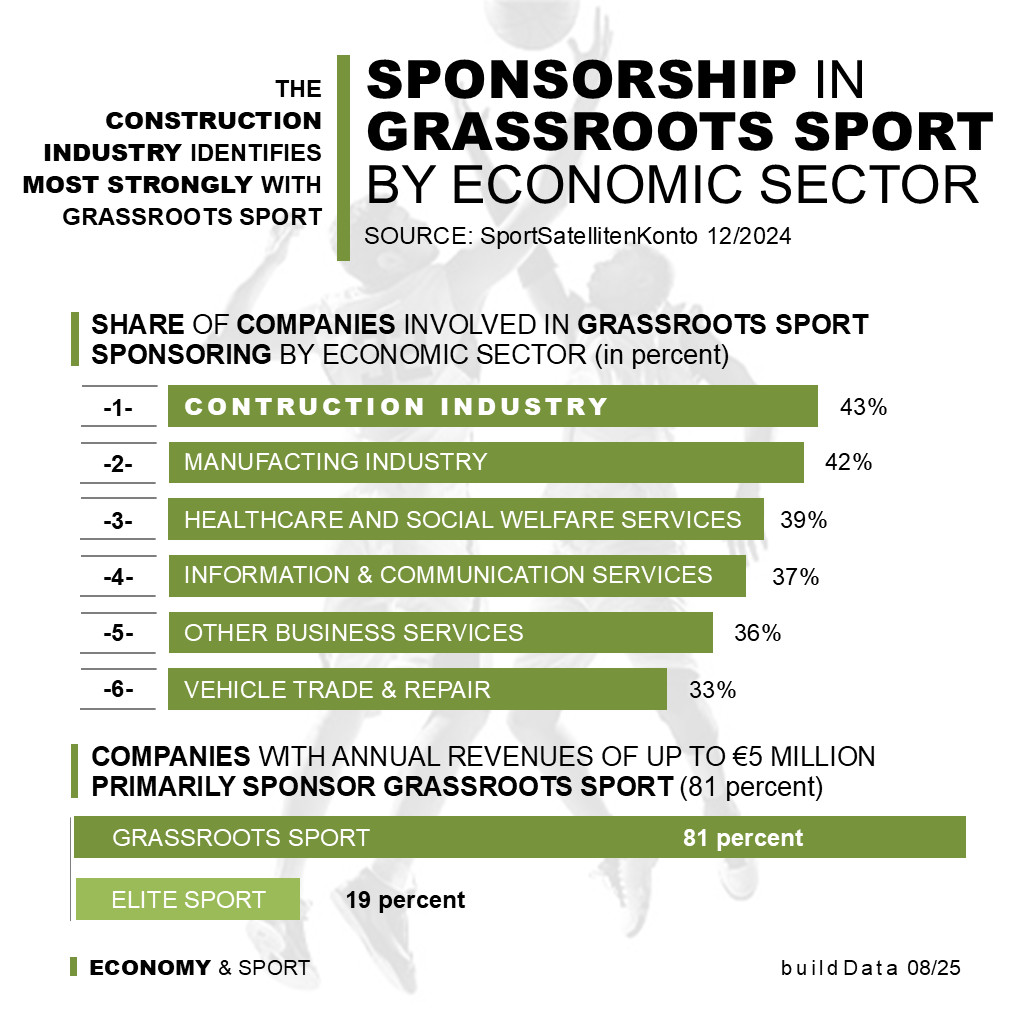

The construction industry is an important partner for amateur grassroots sport

Published

08/2025 by Team buildData

The broad base of companies in the construction industry is mainly involved in sponsoring amateur grassroots sport. Acquiring licences, naming rights or media rights is not important to these companies. For them, the focus is on promoting the sport rather than gaining advertising exposure in return.

More than 4 out of 10 companies from the diverse construction industry sponsor activities in grassroots sport. 81 percent of these companies' sports sponsorship benefits amateur grassroots sport. Interest in professional sports only increases among companies with an annual turnover of more than £5 million.

By far the largest share of sports sponsorship money, 45 percent, goes to amateur sports clubs, 13 percent to sports facilities, 12 percent to professional sports clubs, 11 percent to sporting events, 7 percent to individual amateur athletes and 6 percent to individual professional athletes, 5 percent to sports associations and league organisations, and the remaining 2 percent to other sporting activities.

Grassroots sports clubs without any professional affiliation generate the majority of their annual income from donations. According to information provided by the clubs and an analysis by the German Sport University Cologne, income from donations accounted for around 77 percent of total annual income in 2019 and around 68 percent in 2020 (Covid). Donations are therefore essential for grassroots sports clubs. Sponsorship by companies without the acquisition of licences, naming rights or media rights is classified as a donation in these statistics, together with donations from private individuals.

15 percent of the broad business base in sports sponsorship has no direct connection to sport.

127 of 399 companies involved in sports sponsorship have an annual turnover of over €5 million, 120 between €0.5 and €5 million, and 152 less than €500,000.

Sponsorship funds continue to be unevenly distributed between women's and men's sports. Women's sports account for only 43 percent.

As in the professional sector, football is also the clear focus of sponsorship among the broad business base. Around 31 percent of sponsorship funds go to this sport. Handball accounts for 12 percent, shooting sports for 8 percent and fitness for 6 percent. These are the four largest areas.

29 percent of the companies surveyed stated that their motivation for sponsorship was simply to support sport. However, the main motivations are to improve the company's image (35 percent) and brand awareness (34 percent) and to achieve greater customer loyalty (33 percent). Companies that do not engage in sports sponsorship mainly cite the fact that their budget does not allow for such a commitment.

Sponsorship or donations with the intention of consciously ‘supporting sport’ are therefore not far behind the classic corporate goals of sponsorship. This strengthens the overall system of sport and promotes the breadth of what is on offer, especially in grassroots sport.

When viewed in the context of sport as an overall economic factor, it can initially be noted that the expenditure made directly by companies through sports sponsorship and advertising, including media rights, amounts to approximately €5.5 billion. This is comparatively low when compared to the sports-related expenditure of private households (approximately €82 billion per year) and the investment associated with sports facilities, operating and personnel costs (approx. €27 billion per year).

Open-ended property funds are caught in a downward spiral

Published

01/2025 by Team buildData

At the turn of the year, many of us take advantage of the quiet time to analyse the past and set a new course for the future. In doing so, we always come to the point of our own finances and, ideally, to the question of what is best to invest in. But one thing is clear: property funds are currently not worth investing in?

Who doesn't dream of owning their own property or a further capital investment in another property, and then, of course, at a low cost and in a prime location. It is true that building interest rates have been trending down since mid-2024. In December 2024, interest rates were close to 3 per cent. But material and construction costs remain high.

But there are other ways to invest in property. For example, in property funds. But are property funds an alternative to the currently highly sought-after but perhaps now overheated technology ETFs or ETFs with Amazon and Co.?

You can invest in so-called open-ended and closed-ended real estate funds. First of all, it is important to clarify what the difference is. An open-ended fund is available to everyone at all times, while the units available for purchase in closed-ended funds are limited. Once all available shares have been sold and the marketing period has expired, no further shares can be subscribed. Open-ended funds are a portfolio of several real estate properties and thus represent a lower investment risk than closed-ended funds, which may contain one or a few properties. Closed-ended real estate funds are usually set up with the aim of raising capital to implement a specific real estate project.

Open-ended property funds are classic investment funds that tend to require a low minimum investment amount but do not give investors any voice or decision-making rights. Closed-ended property funds are not listed on the stock exchange, have a limited term and require a high minimum investment. However, the latter generally give investors a limited voice and decision-making rights.

The funds differ particularly in terms of expected returns and risk classification. Open-ended property funds are more broadly diversified and are therefore categorised in risk class 2 ‘Security and interest’ and therefore also have a significantly lower expected return (1.2 %) than closed-ended funds. Not every closed-end property fund is categorised as ‘speculative to highly speculative’ and thus assigned to risk class 7, but many are. A total loss is possible. In addition, such investments only pay off after a longer period of 5, 10 to 15 years. Then, when the risk turns out to be positive, with a high return. Investors are enticed by promises of up to 8% p.a. and a total distribution of 200%, but according to statistics, these often only leave disappointed investors in their wake.

For a long time, open-ended real estate funds were considered a solid and lucrative investment, but financial advisors are currently advising against buying and rather in favour of selling. In recent years, returns have shrunk significantly. The situation in the construction industry is tense. And not least since the high price loss of 17 per cent of its assets in one day at the end of June 2024, the ‘UniImmo’ fund, open-ended real estate funds have been in a downward spiral. Depending on the performance of the funds, the results in 2024 ranged into the slight negative range.

Closed-end property funds are speculative and only suitable for those who can easily absorb a total loss, even in the worst case.

We therefore concur with the relevant financial experts and advise against investing in property funds at present.

Will civil engineering remain on course for growth?

Published

12/2024 by Thomas Hartwig

High-rise construction and residential construction in particular are struggling with higher interest rates, the sharp rise in material and personnel costs, and the increasingly limited financial resources of investors. Not so civil engineering, which is expected to grow by 7.5 percent in Europe between 2024 and 2026. Will it stay on track? And what are the prospects for civil engineering in the UK?

In Germany, this still seems to be the case at the moment. In the first half of 2024, output in civil engineering rose by a total of almost 2 percent. According to the German Construction Industry Association's (ZDB, Zentralverband des Deutschen Baugewerbes e.V. ) half-yearly report, public-sector civil engineering rose by around 0.5 percent, and commercial civil engineering by around 3 percent.

New orders in civil engineering up to July 2024 are seven percent higher than in the previous year, while in commercial civil engineering they are a good 1.4 billion euros above the previous year's level (+11 percent).

Public-sector investments in civil engineering in the first half of 2024 are also higher than in the previous year. Incoming orders as of July are 4.0 percent above the previous year's level. By July, civil engineering revenues are a good two billion euros higher than in the previous year (+12 percent).

A brief comparison with the general construction industry in Germany (half-yearly balance 2024):

- Turnover in the main construction trade January to June 2024: approx. 48.6 billion euros (in real terms minus 2.2 % compared to the same period in 2023)

- Forecast 2024: turnover minus 3%

- Employment: minus 30,000

- New orders for residential construction in the first half of 2024: nominally minus 12.6 percent below the previous year's level (2023)

- Turnover in residential construction: approx. 10.75 billion euros (minus 12 percent)

It is quite clear that civil engineering is benefiting not only in Germany, but throughout Europe, from the pronounced need for action by governments, which arises from political energy and environmental goals, the adaptation of transport infrastructure and the necessity for general network modernization. Thus, the prioritization of these focal points in the national budgets as well as the EU funds (Recovery and Resilience Facility) are playing into the cards of civil engineering. In particular, financial support from the European Union is of great importance for Eastern European countries.

The expansion of rail networks, energy supply infrastructure and investments in telecommunications networks are particularly dynamic for the generally positive economic figures in civil engineering.

And what about civil engineering in the UK?

The BCIS infrastructure forecast 2Q2024 to 2Q2029, published by Dr David Crosthwaite and this team, provides information and predicts a substantial increase in output of 19 percent in the next five years for civil engineering. Over the same period, civil engineering costs will rise by 15 percent and tender prices by 23 percent.

This forecast is based in particular on the new government's activities in the energy sector. Wind energy will receive a boost from extensive offshore and onshore projects. However, the continuation of major projects such as HS2 (UK's high-speed rail network) and EDF's two new nuclear reactors at Hinkley Point C (3,200 MWe) in Somerset also play a role.

The government in London has announced a 10-year infrastructure investment strategy. However, further details are still awaited and are expected in the context of further budget planning.

The global >BESS< Market will grow twofold by 2030

Published

11/2024 by Team buildData

BESS is already a billion-dollar market worldwide and will continue to grow enormously in the coming years. By 2030, investments in battery energy storage systems are predicted to double. In particular, the market for storage capacities for electricity from renewable energies will grow by around 29%.

The expansion targets for renewable energies are ambitious worldwide. However, electricity from the sun and wind also causes problems as it is not permanently available and, for example, is generated in excess during strong wind events or in summer in the midday sun. But we need stable power grids in terms of voltage and frequency. Many renewable energy sources are not plannable, they are volatile and thus represent a burden for the grids. The fluctuations must be balanced and overproductions are lost unused.

Battery storage systems have been identified as a central solution to this problem. They provide the necessary flexibility because the battery storage systems can provide their full capacity in seconds. If there is an excess of electricity from renewable sources, the storage systems absorb it. The technology is so sophisticated that an efficiency level of around 90% can be achieved.

The effective lifespan of large batteries is around 15 years. Thanks to advances in technology over the last 10 years, BESS systems have become 80% cheaper and thus economically viable.

The problem and demand for a stable solution and the fact that battery storage technology has become profitable will have the positive effect of increasing the market to 120 to 150 billion US dollars by 2030.

According to a study by the Fraunhofer Institute for Solar Energy Systems ISE, Germany alone will have to expand its battery storage capacity by a factor of 200 to 104 gigawatt hours by 2030 in order to be able to obtain 80 percent of its electricity from renewable sources. The European Court of Auditors sees Europe as clearly lagging behind in a global comparison of battery storage capacities and therefore calls for a new strategic action plan in the special report 15 (year 2023), with a special focus on ensuring access to sufficient raw materials, the rare earths.

The greatest demand and growth in BESS is expected in the so-called FTM (front of the meter) area, the area of electricity generation and distribution. This is estimated at around 29 percent. The commercial and industrial and residential sub-segments in the so-called BTM (behind the meter) area will each grow by 13 to 14 percent by 2030. This is the result of research by McKinsey & Company.

The key FTM area includes the players involved in renewable energies, developers, utilities and grid operators. Most of the money invested in BESS is still spent on services that increase the flexibility of energy suppliers. In the future, investments will focus on systems and large-scale battery storage that meet the demand for short-term storage of solar and wind energy.

To successfully enter the BESS market, you have to think big and act fast. The market is in a real boom phase, with the major players dynamically positioning themselves in prime locations. At some point, it becomes difficult for smaller developers and technology companies to keep pace or even enter the market.

Construction Output - Turning point expected in 2025

Published

10/2024 by Team buildData

The construction industry in Europe continues to operate in a difficult economic context. A decline of around 2.1% has already been forecast for the Euroconstruct area for the current year 2024. What are the trends for the coming years?

The mood in the construction industry remains gloomy. Above all in the area of building construction, which still covered four-fifths of the construction volume before 2024. Civil engineering, for which steady growth continues to be forecast, accounted for around one-fifth.

The decline in construction output in Europe is due to several economic and structural factors:

The European Central Bank (ECB) has raised key interest rates in recent years to curb inflation, which has led to higher financing costs for construction projects. Mortgages are becoming more expensive, which reduces the demand for residential real estate, while the demand for it remains high. There is a housing shortage, particularly in the lower price segment. Under these conditions, however, investors are hesitant to initiate construction projects.

Added to this are rising wages, a shortage of skilled workers and the sharp increase in material costs since the beginning of the COVID-19 pandemic and as a result of geopolitical tensions. Particularly noteworthy here is the conflict in Ukraine. The prices for steel, concrete and wood are at an expensive level.

In relation to Germany, the economy is falling deeper into recession. Current figures place the German economy at the bottom of the G7 states.

However, there are regional differences in Europe. This is also reflected in the outlook for construction output in the coming years, for which a modest recovery is expected for the Euroconstruct area.

The Scandinavian countries Finland, Sweden and Norway are forecast to see a healthy increase of up to 7.5% (Finland, 2025) and 6.0 to 6.7% (Sweden, 2025 and 2026), while only a slight recovery from -3% and -3.7% in 2024 to around -0.2 to +0.7% in 2026 is expected for Germany and France.

The construction industry in Poland has been continuously growing for three years. Coming from +3.5% in 2021, +5.9% in 2022, and between +3.9 and +3.5% in 2023 and 2024, growth of +5.0 and +6.0 percentage points is forecast in 2025 and 2026.

The UK came from a difficult year in 2020 with a big minus of 14.2% to a big plus of 11.7% in 2021. It fell back to -0.6 percentage points in 2024, but is expected to grow by +4.1% and +2.5% in 2025 and 2026.

As already mentioned, residential construction remains a problem area. A decline in the completion of residential units of around 17% is forecast for the entire Euroconstruct area between 2022 and 2026. France, Germany, the UK and Poland are the strong markets in this area. In 2022, around 1.1 million residential units were built in these countries. By 2026, there will only be around 880 thousand completions.

There will be no significant impetus in the commercial sector, while civil engineering will continue to grow between 2024 and 2026. This will probably be the case in all sub-sectors without exception. More on this in a further article shortly.

Rare earths

Published

10/2024 by Thomas Hartwig

15 lanthanides, as well as scandium and yttrium, are the essential chemical elements for numerous key technologies. They are called rare earths. They are used in electric motors, wind turbines, semiconductors, screens, batteries and other high-tech applications.

The term rare earths is not based on the widespread belief that they are rare in occurrence. The metals are relatively abundant in the earth's crust. However, they are widely dispersed and rarely found and extracted in economically viable concentrations. High concentrations and thus favorable mining conditions are found in China.

China has the world's largest deposits and reserves and dominates world production, accounting for approximately 70 percent. Other significant mine production is located in the United States, Burma and Australia. In 2023, 43,000 metric tons were mined in the United States, 38,000 metric tons in Burma and 18,000 metric tons in Australia. By comparison, China mined 240,000 metric tons in 2023.

China also holds the leading position in global reserves. The country has estimated reserves of 44 million metric tons. Large deposits are located in Inner Mongolia. The USA has only 1.8 million metric tons left and already imported 72 percent of rare-earth compounds and metals from China between 2019 and 2022.

The distribution of rare earths has geopolitical implications. Myanmar, formerly known as Burma, has the world's second-largest reserves of rare earths and plays a significant role in China's strategic considerations in Southeast Asia. The dependency of Western countries is becoming apparent and entails supply risks.

In addition to the risks of dependency, there are also other issues surrounding rare earths. The mining and processing of rare earths often has a significant environmental impact. Due to the issues of dependency and the environment, efforts are being made to strengthen the circular economy in order to recover rare earths through recycling, for example from batteries, permanent magnets and fluorescent lamps.

Bureaucracy weights on German entrepreneurs

Published

10/2023 by Thomas Hartwig

On average, the permit process for the construction of wind turbines in Germany takes 24.5 months. Is that still in keeping with the times?

Bureaucracy is supposed to help make procedures transparent and fair for everyone and build trust in making decisions. However, it is obviously becoming more and more of a burden, especially for medium-sized companies.

Medium-sized companies name bureaucracy as their number one concern. While entire departments in large companies deal with which new legal regulations for business or, for example, permits must be complied with, medium-sized companies simply lack the human and financial resources to do so.

Although the bureaucracy index in Germany has fallen from 2012 (100) to 98.5 (2023), small and medium-sized companies feel that dealing with government offices, chambers and authorities is increasingly or very burdensome. This impression is not surprising in view of the index trend in recent years. In 2022, it was still just below the value of 97.

55 percent of family businesses state that bureaucratic costs are the biggest barrier to investment for them. Many small companies therefore do not even tackle certain projects because of the bureaucratic hurdles. Innovative projects are often affected.

But even simple projects, such as the founding of a startup or company, seem to test the patience of the founders. More than 70 percent of the founders surveyed said that forms and processes for founding a company were too complex and that requests were processed too slowly.

68 percent of entrepreneurs in Germany say they have already had very bad experiences with bureaucracy.

There is no denying that the reduction of bureaucracy needs to gain noticeable momentum, especially for small and medium-sized enterprises. Germany wants to achieve many things in the coming years and decades and remain internationally competitive. First and foremost in the areas of energy, mobility, AI and digitization. To this end, the innovative SME sector in particular needs to be relieved of bureaucracy.

How to counter rising damage costs in civil engineering

Published

09/2023 by Thomas Hartwig

Damage repair costs in civil engineering increase by 24 percent within 5 years.

This is shown by the Construction Damage Report for Civil Engineering and #Infrastructure of the VHV insurers. Almost 40,000 claims were examined in the period between 2017 and 2021. The focus on the average costs per claim and year is even more pronounced, with an increase of 31 percent.

Most claims occur in line construction. 57.5 percent of the damage to lines is caused by the use of working machines and 19.7 percent by execution and installation errors. Communication lines are by far the most affected or damaged type of line.

Inaccurate and incomplete site plans were identified as the cause of damage by around 95 percent and imprecise planning information by around 88 percent.

The motivation to contain a further increase in damage repair costs, for example through the introduction of a central line cadastre, is great, especially since the risk of damage occurrence should increase significantly with a focus on digitalisation, the energy and transport transition and the resulting increasing density of the network structure in the future.

Lack of Orders

Published

09/2023 by Thomas Hartwig

Residential construction in Germany continues to cool down. – Cancellations are increasing drastically, new business is almost at a standstill.

According to the Ifo Institute, the real estate market in #residential construction continues to head for a severe crisis. According to the latest survey, more than 18.9 per cent of construction companies in the residential construction sector complained about cancellations of scheduled projects in July 2023. In the previous month of June 2023, the figure was 19.2 per cent. Compared to the long-term average of 3.1 percent, these are drastic figures.

High interest rates coupled with high material and #construction costs are to blame for the development. New business is strangled under these conditions.

In July 2023, more than 40 percent of construction companies in the residential construction sector complained about a lack of orders. That is one in four out of ten companies. In June 2023, it was already around 34.5 percent. Compared to the previous year, this percentage has roughly quadrupled.

While many companies are still drawing on order backlogs from better times, every tenth company is now already in crisis mode. In the current survey, 10.5 percent of the companies say they are already experiencing financing difficulties.

According to the survey, companies in the residential construction sector are extraordinarily pessimistic about their business prospects, scoring minus 51 points.

With a focus on the politically set goal of meeting the high demand for affordable housing in particular, the framework conditions must be readjusted by politicians. Otherwise, housing construction will be in free fall within a very short time.

Investment in Green Buildings

Published

04/2023 by Thomas Hartwig

Here is a brief update on the topic of building and sustainability.

In recent months, we have reported in various posts on the topic of green buildings. Now, research by BNP Paribas Real Estate and last weekend’s report in Handelsblatt confirms the growing interest in investing in buildings constructed to the highest sustainability standards.

In 2022, the share of transactions in certified properties increased by 4.9% year-on-year to a total of 30.6%. In office properties, a peak value of 46.2 % was reached, so that almost every second newly constructed office building is a green building. In the logistics sector, the share rose from 16.5 % (2021) to 27 % (2022).

The demand for sustainable real estate is particularly high among institutional investors, such as insurance companies and pension funds as well as open-ended funds. The focus is on the so-called A-cities Berlin, Düsseldorf, Frankfurt am Main, Hamburg, Cologne, Munich and Stuttgart.

Green buildings are properties in which attention is paid to a maximum reduction of CO2 emissions in the planning, design, construction, operation and also the subsequent deconstruction (reuse of materials). This is assessed in so-called life cycle assessments. Among other things, EPDs (Environmental Product Declarations) for the classification of building products form the basis.

The technical development of green buildings will continue to be dynamic. As already reported, example projects have shown that even simple changes in structural design, away from conventional construction methods, can lead to additional CO2 savings of up to 30%.

With the growing importance of sustainable real estate, the pressure is increasing to create more incentives for this as well, since this savings potential is currently not yet taken into account in the ESG criteria.

The offer price is and remains decisive

Published

12/2022 by Thomas Hartwig

A survey by the Baden-Württemberg Chamber of Engineers makes it clear that engineering firms are no longer satisfied with the award processes of public clients.

With the introduction of the HOAI 2021 (Honorarordnung für Architekten und Ingenieure), the fees for planning services are no longer bound to a fixed framework, which obviously leads to problems and quality losses in the implementation of contracts.

Thus, 18% of the respondents stated that the price had been the decisive criterion for the award of the contract in over 90% of their submitted bids. For 64% of the respondents, the price criterion was decisive in over 70% of the bids submitted. 52% of the survey participants also stated that the potential clients had expected a price reduction below the base rates.

The possibility of flat-rate discounts resulted in price reductions of around 30% below the base rates on several occasions.

On top of that, for many of the respondents the award processes are not very transparent. 82% of the respondents state that they have not to receive sufficient justification for their rejection. This is certainly one reason why around 78% of respondents consider it rather useful to publish the evaluation and decision matrix in the public procurement procedures.

The public contracting authorities are called upon to make improvements. The result of the survey cannot be understood in any other way. After all, the effort required to process the bids is not small. 83% of the engineers state that the effort required for the award procedures is rather inadequate or must be rated as much too high.

Surprisingly, the digitalisation of the award procedures is to blame for the increased effort. Actually intended as a simplification, electronic awarding apparently has the opposite effect.