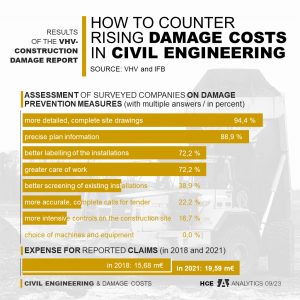

Will civil engineering remain on course for growth?

Published

12/2024 by Thomas Hartwig

High-rise construction and residential construction in particular are struggling with higher interest rates, the sharp rise in material and personnel costs, and the increasingly limited financial resources of investors. Not so civil engineering, which is expected to grow by 7.5 percent in Europe between 2024 and 2026. Will it stay on track? And what are the prospects for civil engineering in the UK?

In Germany, this still seems to be the case at the moment. In the first half of 2024, output in civil engineering rose by a total of almost 2 percent. According to the German Construction Industry Association's (ZDB, Zentralverband des Deutschen Baugewerbes e.V. ) half-yearly report, public-sector civil engineering rose by around 0.5 percent, and commercial civil engineering by around 3 percent.

New orders in civil engineering up to July 2024 are seven percent higher than in the previous year, while in commercial civil engineering they are a good 1.4 billion euros above the previous year's level (+11 percent).

Public-sector investments in civil engineering in the first half of 2024 are also higher than in the previous year. Incoming orders as of July are 4.0 percent above the previous year's level. By July, civil engineering revenues are a good two billion euros higher than in the previous year (+12 percent).

A brief comparison with the general construction industry in Germany (half-yearly balance 2024):

- Turnover in the main construction trade January to June 2024: approx. 48.6 billion euros (in real terms minus 2.2 % compared to the same period in 2023)

- Forecast 2024: turnover minus 3%

- Employment: minus 30,000

- New orders for residential construction in the first half of 2024: nominally minus 12.6 percent below the previous year's level (2023)

- Turnover in residential construction: approx. 10.75 billion euros (minus 12 percent)

It is quite clear that civil engineering is benefiting not only in Germany, but throughout Europe, from the pronounced need for action by governments, which arises from political energy and environmental goals, the adaptation of transport infrastructure and the necessity for general network modernization. Thus, the prioritization of these focal points in the national budgets as well as the EU funds (Recovery and Resilience Facility) are playing into the cards of civil engineering. In particular, financial support from the European Union is of great importance for Eastern European countries.

The expansion of rail networks, energy supply infrastructure and investments in telecommunications networks are particularly dynamic for the generally positive economic figures in civil engineering.

And what about civil engineering in the UK?

The BCIS infrastructure forecast 2Q2024 to 2Q2029, published by Dr David Crosthwaite and this team, provides information and predicts a substantial increase in output of 19 percent in the next five years for civil engineering. Over the same period, civil engineering costs will rise by 15 percent and tender prices by 23 percent.

This forecast is based in particular on the new government's activities in the energy sector. Wind energy will receive a boost from extensive offshore and onshore projects. However, the continuation of major projects such as HS2 (UK's high-speed rail network) and EDF's two new nuclear reactors at Hinkley Point C (3,200 MWe) in Somerset also play a role.

The government in London has announced a 10-year infrastructure investment strategy. However, further details are still awaited and are expected in the context of further budget planning.